Market Outlook

Introduction

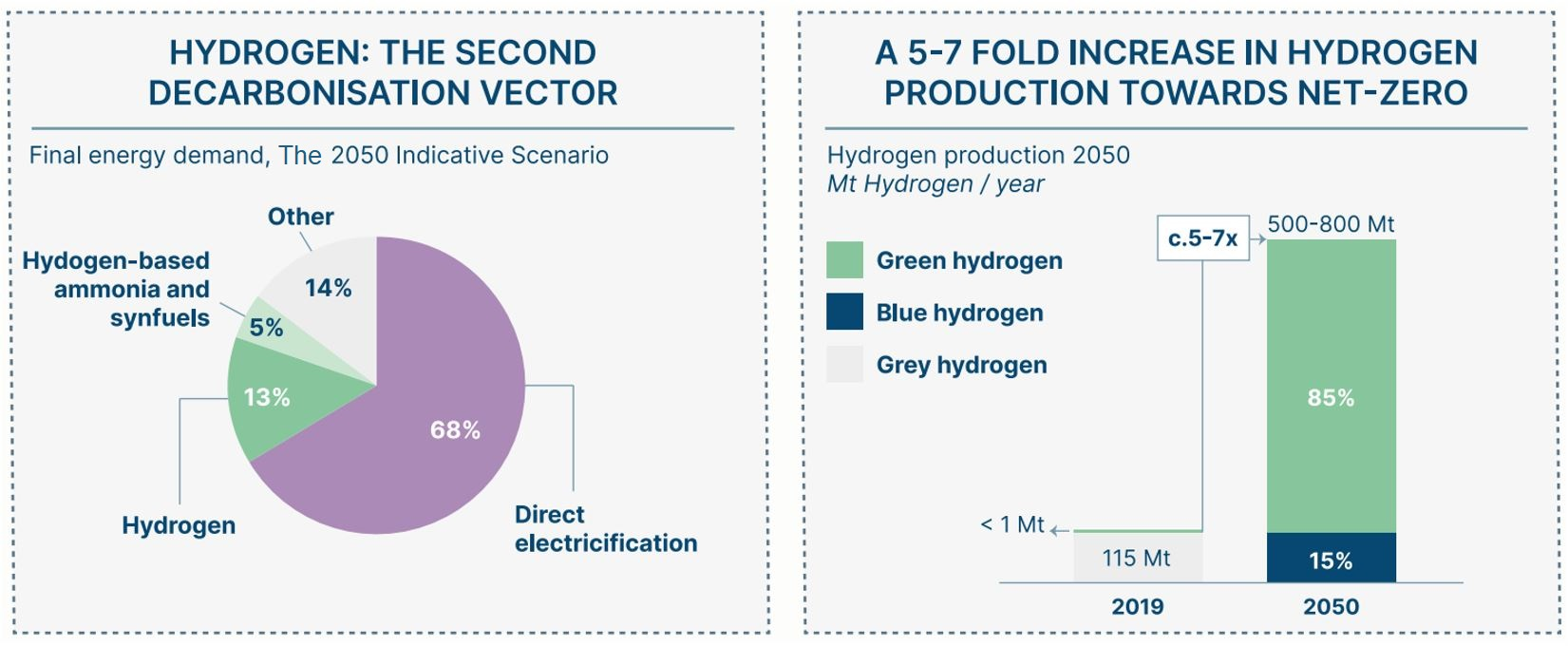

Clean electrification must be at the core of all initiatives aimed at achieving a zero-carbon economy, with electricity being used in substantially more applications than in present, and all power being produced in a carbon-free manner. Electrification is, without a doubt, the most cost-effective approach to meet most energy demands. Clean electrification can cut total energy system costs while simultaneously delivering significant local environmental advantages, both to lower all-in generating costs and the natural efficiency gain associated with a conversion to electricity. According to the most recent research on the global power system, direct electricity consumption might and should increase from 20% of total final energy demand today to close to 70% by 2050, with electricity generation to enable direct electrification increasing from 27,000 TWh to 90,000 TWh.

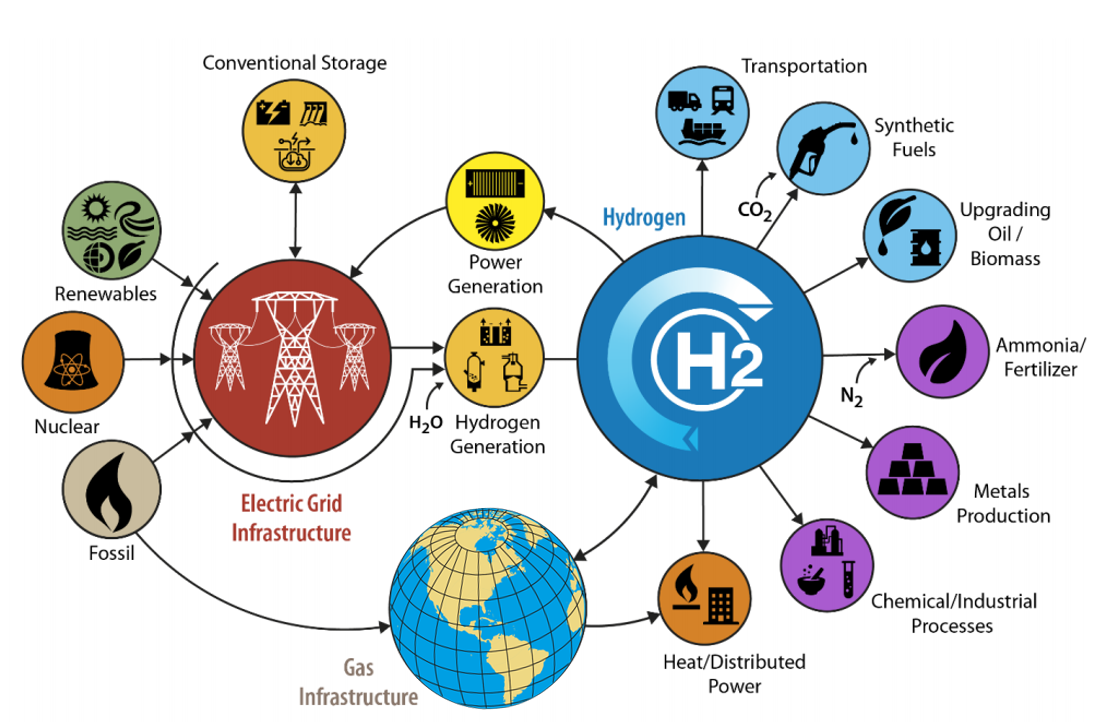

Direct electrification, on the other hand, will likely remain unfeasible or uneconomic in some areas for decades. In several of these, hydrogen, whether utilized directly or in the form of derived fuels like ammonia and synthetic fuels, can play a significant part in decarbonization (synfuels). Hydrogen's critical new position in steel and long-distance shipping, for example, is becoming increasingly definite; it will continue to be essential in fertilizer manufacture, and it is one of the top decarbonization choices in a variety of other sectors. Hydrogen will play a major role in future electrical networks as an energy storage device, helping to balance supply and demand in systems that rely heavily on variable renewable energy (VRE) sources.

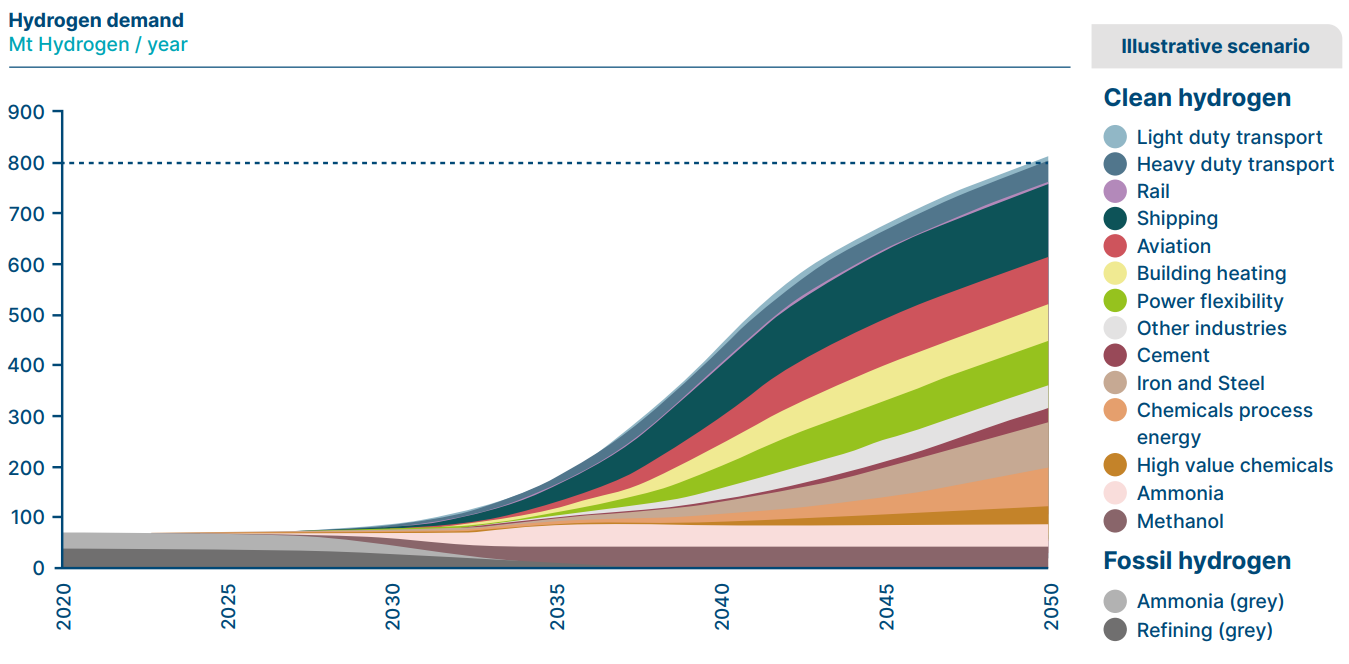

Total worldwide hydrogen consumption might thus increase 5-6-fold by 2050, from 115 Mt per year to 500 to 800 Mt, with hydrogen (and its derivatives) accounting for 15-20% of final energy demand, on top of the close to 70% delivered by direct electricity. If implemented in a manner that achieves near-total CO2 capture and very low methane leakage, all of this hydrogen must be produced in a zero-carbon manner via electrolysis using zero-carbon electricity or in a low-carbon manner using natural gas reforming + CCS (blue hydrogen). During the transition, blue hydrogen will typically be more cost-effective than grey hydrogen, particularly when retrofitting existing grey hydrogen, and in the long run, in areas with very low gas costs.

Green hydrogen, on the other hand, will be affordable in most places in the long run, with lower production costs. Hydrogen production will thus be primarily green and will produce a considerable amount of power demand, potentially boosting the total required supply of zero-carbon electricity by 30,000 TWh or more on top of the 90,000 TWh needed for direct electrification. Green hydrogen plays a vital role in achieving net-zero emissions by mid-century in both industrialized and developing countries, and the consequences for required clean electricity supply – which is technically and financially achievable.

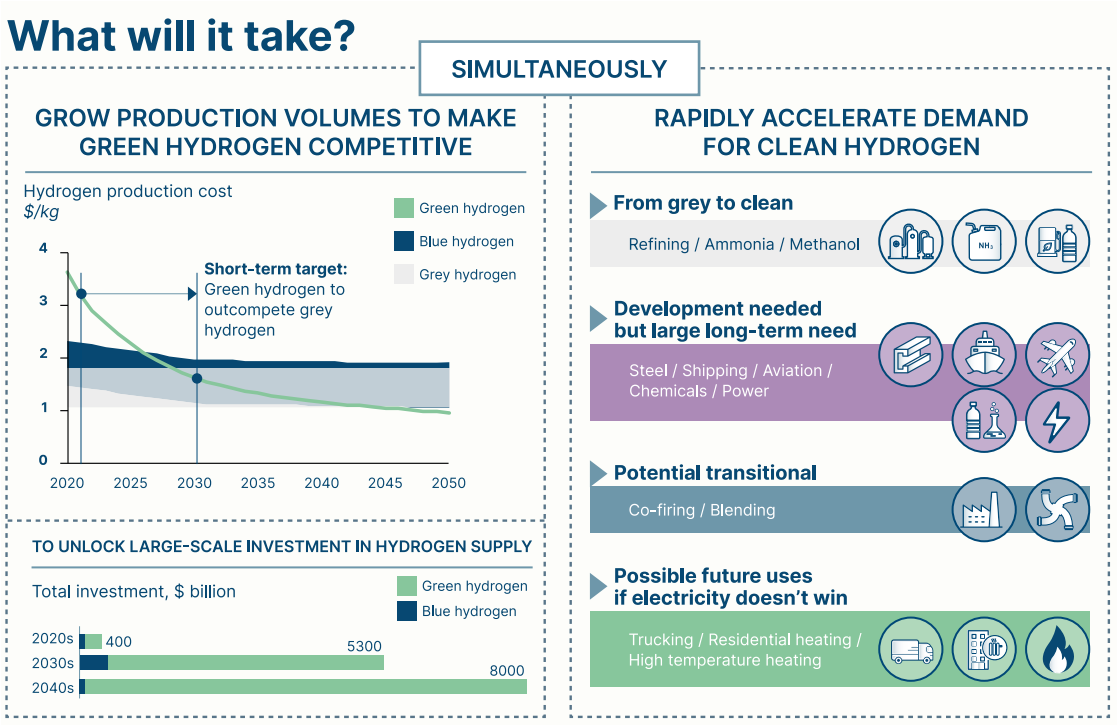

In order to meet the 2050 targets, hydrogen production and use must take off as soon as possible. It will take legislative support to do this since, even if clean hydrogen production prices fall significantly, employing hydrogen in end applications frequently comes with a green premium (compared to fossil fuel technologies). These strategies must combine broad policy instruments like carbon prices with assistance for specific industry applications and the creation of geographically localized clusters of clean hydrogen production and usage.

Hydrogen is certain to play a significant role in the transition to a carbon-free economy. It can be used to decarbonize key processes in difficult-to-abate transportation and heavy industry sectors where direct electrification is difficult, expensive, or unattainable. Within the power system, it can also serve as an energy storage mechanism. As the cost of producing clean hydrogen declines, it will become more cost-effective than carbon capture and storage (CCS) or bioenergy-based decarbonization options.

Potential Demand Growth

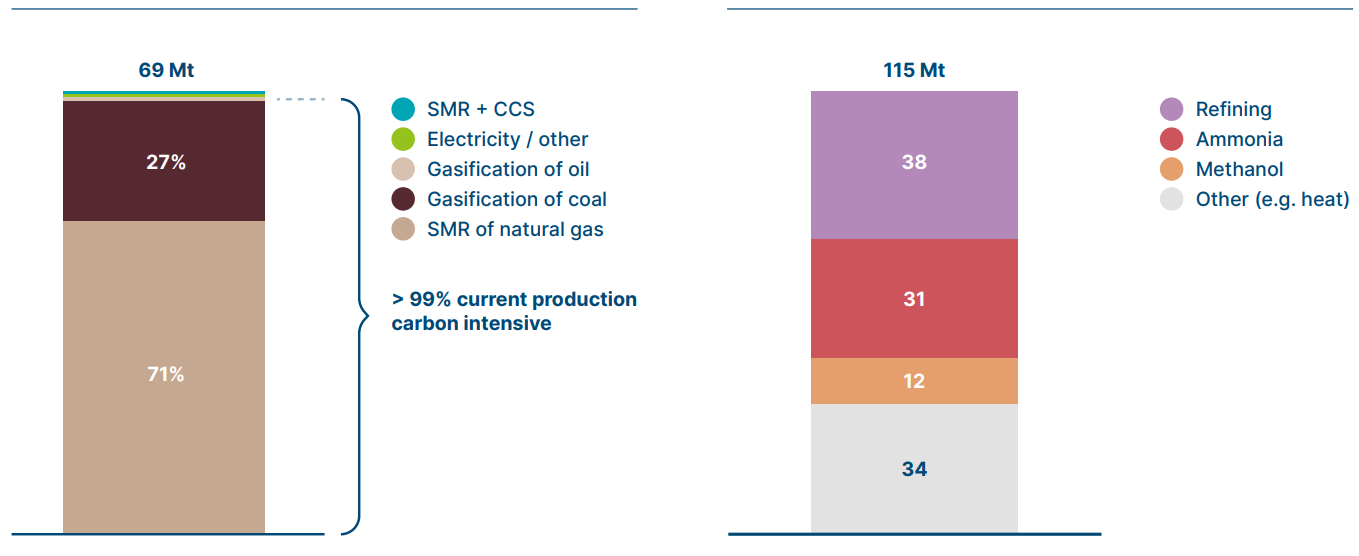

Around 115 Mt of hydrogen was consumed globally in 2018, with 70 Mt coming from dedicated production, primarily from natural gas (71%) and coal (27%). Around 830 Mt of CO2 was emitted as a result of this output, accounting for around 2.2 % of global energy-related emissions. This hydrogen was mostly used in refining (38 Mt), ammonia production (31 Mt, primarily for fertilizer manufacture), and methanol production (12 Mt, used mostly as a fuel additive and for plastics production).

Hydrogen use is expected to grow rapidly over the next three decades, with clean hydrogen replacing hydrogen obtained from uncontrolled fossil fuels in existing applications and being deployed in a variety of new applications. In some industries, the exact role it plays in comparison to other decarbonization strategies (particularly direct electrification) is intrinsically unknown. However, realistic scenarios estimate that a zero-carbon economy in 2050 will require between 500 and 800 Mt of hydrogen per year (see Figure 1).

The production of hydrogen nowadays is based on carbon-intensive methods, with hydrogen being used primarily in the refining, ammonia, and methanol industries.

Dedicated hydrogen production pathways used (2019) Hydrogen use sectors (2019)

% Of dedicated production Mt H₂

Hydrogen use sectors (2019)

Mt H₂

Figure 1

Due to energy conversion losses, hydrogen is often less efficient as an energy source than direct electrification.

In long-distance transport applications, however, the higher energy density per mass of hydrogen and hydrogen-derived fuels such as ammonia or synthetic fuels would exceed this disadvantage. Furthermore, while the conversion/reconversion of electricity to hydrogen results in significant losses, hydrogen provides a cost-effective and practical option to store vast amounts of energy over time.

Because of its chemical properties and reactivity, hydrogen is an essential chemical agent or feedstock in the production of ammonia and methanol, as well as a potential role in the production of plastics and steel.

Likely Applications by Sector

Hydrogen's potential usage in a zero-carbon economy can be divided into four categories:

- Existing hydrogen applications provide clear short-term prospects for a switch to clean hydrogen, as well as a high degree of confidence about long-term demand;

- Uses that will take time to develop but are assumed to be in high demand in the long run;

- Transitional opportunities, even for the short-term;

- Future applications where relative costs and benefits to direct electrification and other decarbonization techniques are unknown.

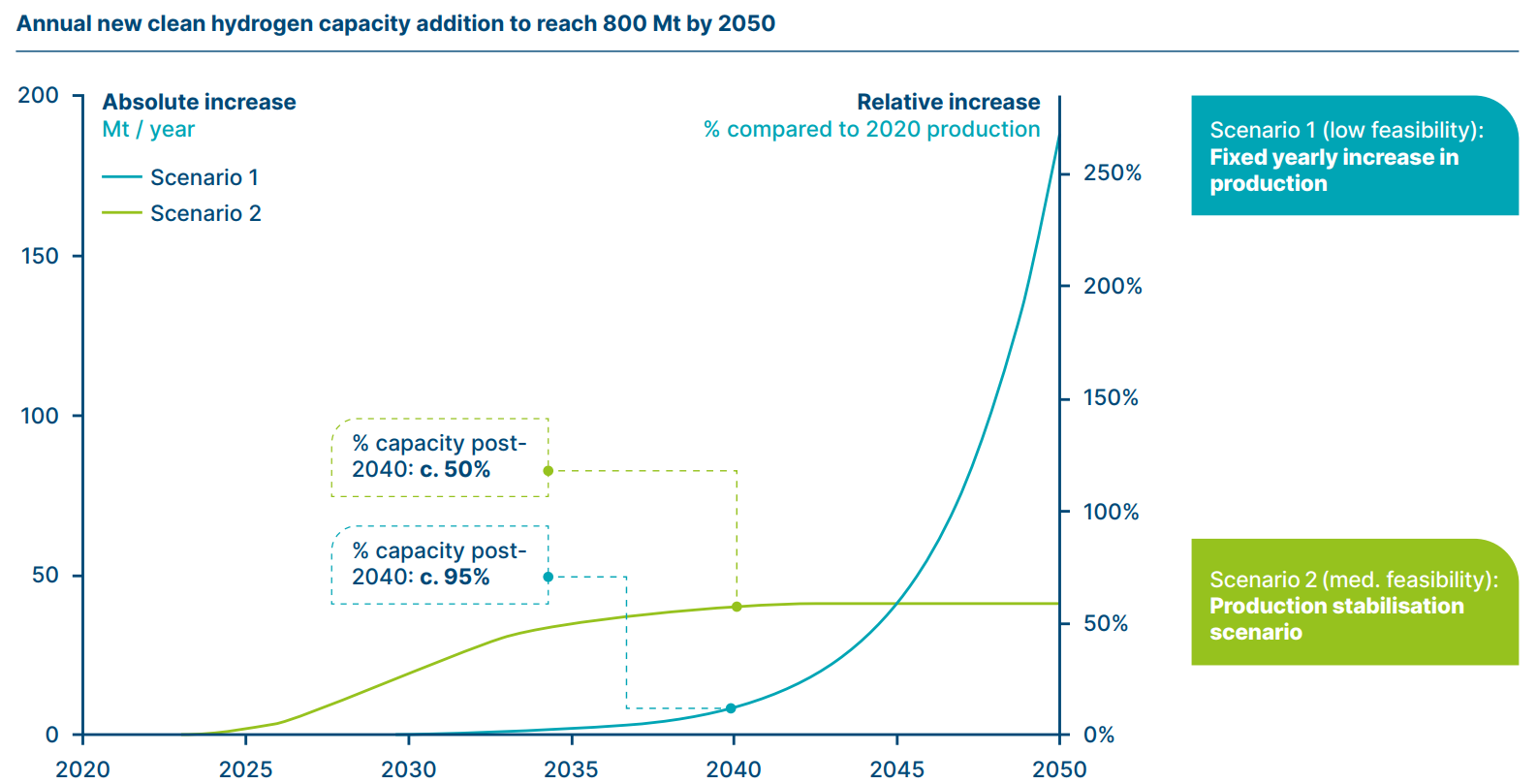

Early and sustained capacity increases are required for a sustainable production ramp-up, with 35 Mt/year production added by the mid-2020s.

NOTE: Scenario 1 curve assumes constant year-on-year growth of 35%. Scenario 2 uses S-Curve logistic equation

Driving Early Demand

Early demand growth for clean hydrogen will be key to accelerating projects in the 2020s, enabling fast cost reductions and putting clean hydrogen on a scale-up path that will allow it to play a role in a mid-century net-zero economy. Employing hydrogen in many end-use applications would still represent a green cost premium. As a result, public policy assistance will be required to push clean hydrogen demand forward.

Specific actions are necessary, with the following primary objectives:

- Ensure that all existing hydrogen production (particularly in oil refining and ammonia production) is rapidly decarbonized.

- Accelerate technology development and early adoption of hydrogen in other major sectors with low technology readiness but high prospective demand, such as steel production and shipping, to enable speedy take-off in the 2030s.

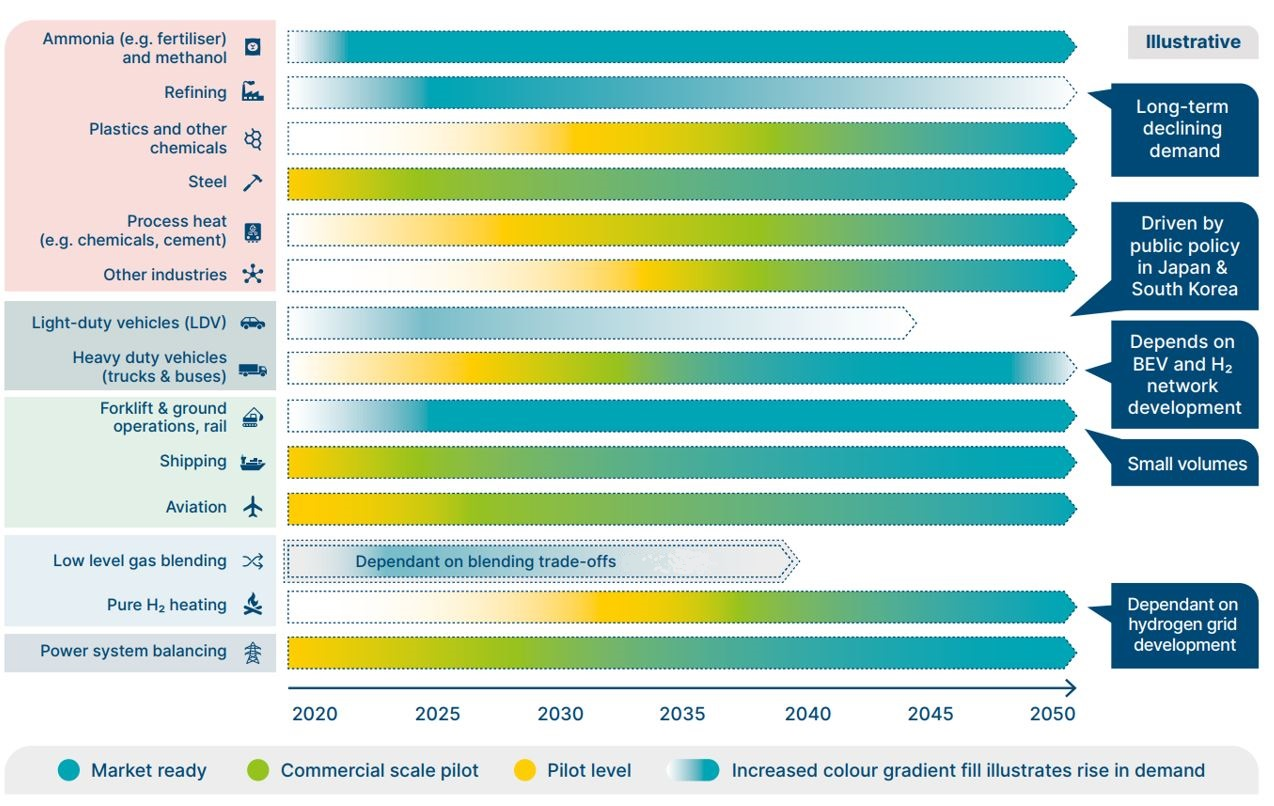

The timing of expansion by sector will be determined by a number of factors, including technology readiness, sector-specific decarbonization pressure, economics verses alternatives, and the extent to which applications rely on the development of new distribution networks. Figure 10 depicts a possible time sequence, with existing applications of grey hydrogen in fertilizers and refining creating immediate potential demand for clean hydrogen – with fertilizer demand likely to grow over time, but refining demand eventually declining as oil use declines.

Demand Sector "Take-Off" Sequences in the Next Future

Figure 10

- Heavy-duty road, rail, and captive transport applications are generating early demand, but the final scale will be determined by the uncertain future balance between battery and hydrogen-based long-distance heavy-duty trucking, as well as the development of hydrogen distribution and refueling systems.

- Steel and long-distance shipping will create significant potential demand from 2030 onwards, but pilot facilities and early commercial-scale investments will occur sooner.

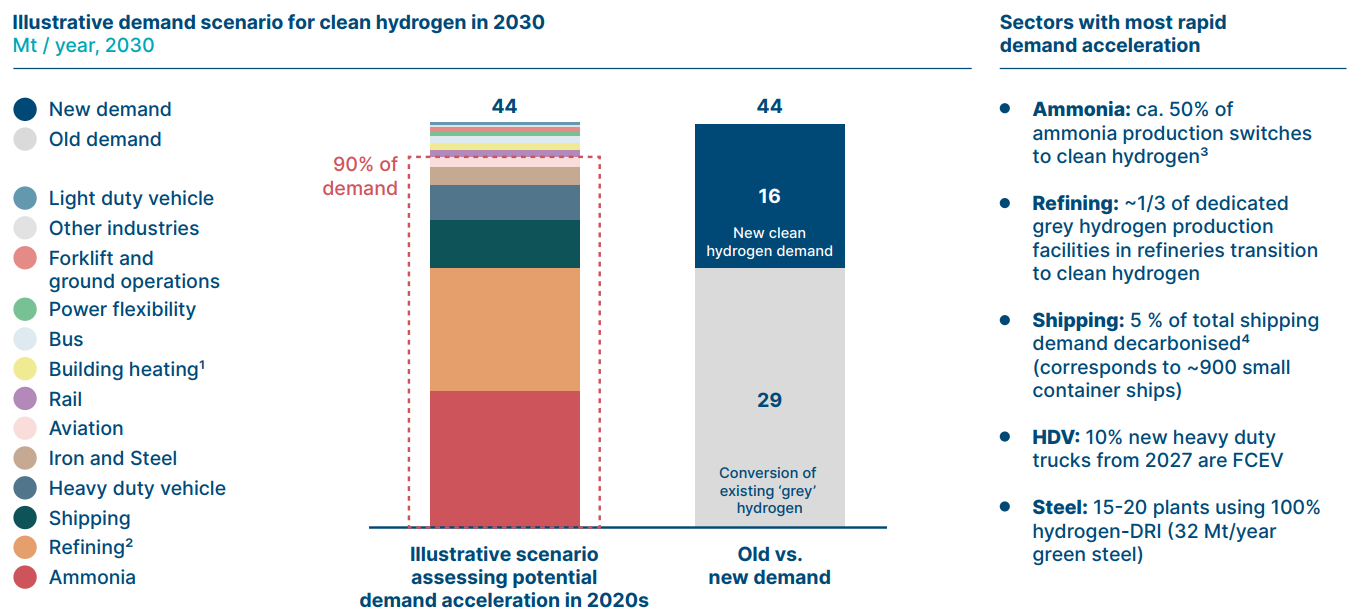

Figure 11 depicts a collection of hypothetical sectoral hydrogen consumption scenarios that would result in clean hydrogen demand reaching 43 Mt by 2030.

Figure 11

NOTES: ¹ Illustrates use of hydrogen in residential and commercial building heating. The dominant form of this in the 2020s is likely gas grid blending. ² Clean hydrogen demand in the refining category summarises existing uses in desulphurisation and in hydrocracking of crude oil. In addition, methanol production, heat provision in chemical industry and production of high value chemicals was also included in this category for this analysis. ³ Ammonia production for use in the chemical industry and ammonium and nitrate-based fertiliser production can transition to clean hydrogen without significant retrofit. Urea production (50%+ of today’s fertiliser production) is more challenging to convert to clean hydrogen. ⁴ This demand would correspond to ca. 900 small container ships

In 2030, an illustrative scenario analyzing potential demand acceleration in present estimates that clean hydrogen consumption will be around 45 Mt, which will necessitate mobilization across five critical industries.

Figure 12

Key Actions to Enable Production Ramp-Up

There are no fundamental barriers to ramping up clean hydrogen production in line with the demand growth depicted in Figure 12, but it is critical to predict the number of expenditures necessary, as well as to identify and remove some barriers to clean hydrogen production development. Green hydrogen production is increasing. Natural resources are sufficient to enable enormous green hydrogen expansion, but the development of the hydrogen value chain will necessitate massive increases in zero-carbon electricity supply and the foresight of new supply chains:

- Minerals: Future demand for key minerals used in the production of alkaline electrolyzers suggests that there will be no long-term restrictions. Only a third of known deposits would be needed to produce all 800 Mt of hydrogen per year using electrolyzers made with primary nickel. Because the present iridium and platinum supply can only support 3-7 GW of yearly production, other materials and lower material intensity will be required for the PEM technology to scale. Electrolyzer recycling and 'designed-in' circularity can help to lessen the need for new minerals. However, it is important to forecast the timing of mineral demand growth, which will be fueled by both hydrogen and direct electrification.

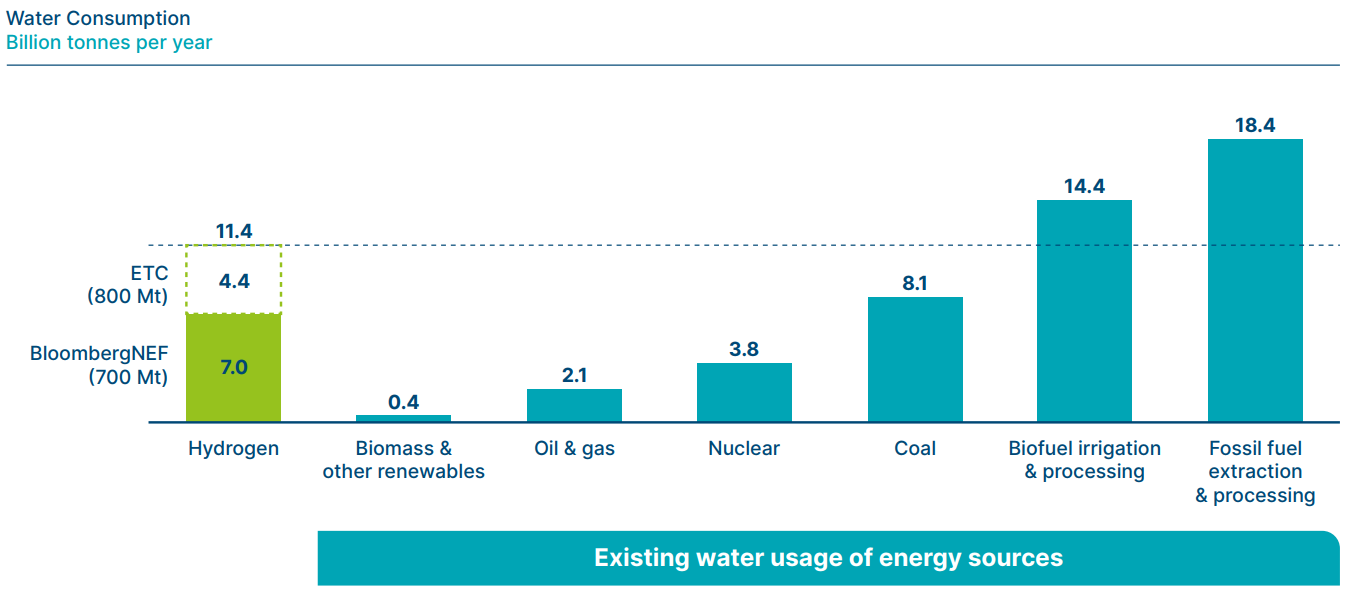

- Water: Despite the fact that each kilogram of hydrogen produced requires a significant amount of water (up to 15-20 kg, including cooling), the water requirements for 800 Mt hydrogen per year are much lower than those for extracting and processing fossil fuels today (Figure 13) and would account for only about 0.7 % of global freshwater use. Desalination can also be used in areas where there is a scarcity of water.

- Electricity: Green hydrogen production will contribute greatly to the large increases in electricity supply that will be necessary for direct electrification in any scenario. In addition to the 90,000 TWh presumably necessary in any scenario for direct electrification, producing 85 % of the 800 Mt hydrogen per year via electrolysis would require around 30,000 TWh of zero-carbon power generation. This large increase in zero-carbon energy (mainly from renewables) is possible, but it will require supportive policies and investments ahead of time. As a result, international strategies for the expansion of zero-carbon power generation, as well as the accompanying transmission and distribution networks, must account for these massive increases.

- Supply chains development: The creation of large new supply chains for critical materials and capabilities – for electrolysis and variable renewable energy generation – will be required to scale clean hydrogen production. These developments are physically doable in the timeframe required, but failure to plan ahead of time could result in bottlenecks, both locally and worldwide, slowing progress and increasing expenses. Only 0.2 GW of electrolyzers were installed globally in 2020; nevertheless, annual additions will need to reach over 30 GW per year by the late 2030s.

Water availability is not a global limiting factor for the deployment of hydrogen production at scale

Figure 13

NOTE: The estimated water consumption for hydrogen is calculated for 100% production from water electrolysis. Other renewables include wind, PV, geothermal and solar thermal, and excludes hydropower. Fossil fuel and biofuel numbers represent water consumption during primary energy production. All other numbers (except hydrogen) represent water consumption during power generation.

Improving Transportation and Storage Infrastructure

Encouragement of early innovations within hydrogen clusters will lessen the reliance on substantial new investments in hydrogen transportation infrastructure for the clean hydrogen economy's early take-off. The expense of transporting hydrogen can add a significant amount to the delivered cost. However, more extensive hydrogen distribution networks may be required in the future, allowing for more scattered hydrogen production, storage, and use.

Partially upgrading existing gas networks to support hydrogen transport is expected to be one of them. Storage investments will become more necessary over time, especially if hydrogen begins to play a larger role in achieving seasonal balance in the power system.

Given the disparities in the availability of large-scale geological hydrogen storage, government-level strategic planning for these infrastructure investments will be required. National policies should also evaluate whether they want to be a hydrogen exporter or a hydrogen importer, and create international partnerships appropriately.

As a consequence, the value of transportation and storage infrastructure is projected to rise over time. Moreover, infrastructure investments could equal or exceed those required for green/blue hydrogen production assets, while remaining significantly lower than those required to build the zero-carbon electricity generation capacity necessary to support a massive scale-up of green hydrogen production. This investment, however, will be far less than the large-scale transportation investments required for today's international fossil fuel trade.

Targets for 2025 and 2030

Due to the small scale of clean hydrogen deployment today (less than 1% of dedicated production), a substantial acceleration is required to enable the hydrogen economy to scale up. Targets for the overall development of production, transportation, and demand can assist unlock a self-reinforcing cycle of private investment for each step of the value chain by giving investors more assurance. These goals must be defined at the national level, but the orders of the magnitude required can be demonstrated at the global level. Over the next decade, a large increase in clean hydrogen production and consumption is required — globally, by 2030:

- By 2030, clean hydrogen production should exceed 50 Mt, lowering average clean hydrogen production costs in all regions and putting capacity expansion on track to meet 2050 targets.

- The majority of the equivalent demand (60 percent or more) should come from decarbonization of existing hydrogen uses, as well as early scale-up of major new hydrogen uses in transportation and industry.