Applications of Green Hydrogen

Applications of Green Hydrogen

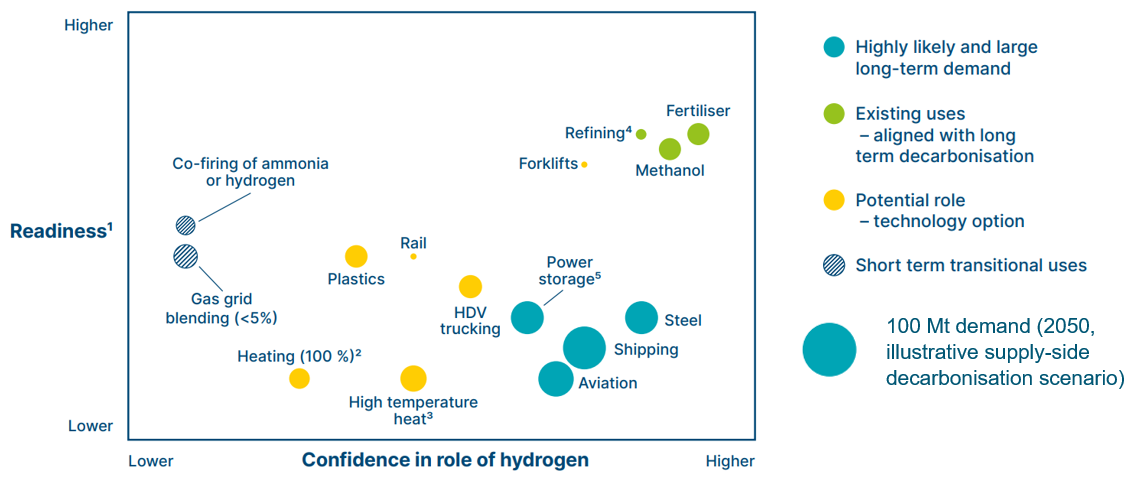

There are multiple potential applications for hydrogen in a low-carbon environment, some of which can provide early off-take for clean hydrogen.

Applications of Kireina Suiso Green Hydrogen

Through hydrogen injection into the existing gas distribution network, the green hydrogen generated at Kireina Suiso can be used as a fuel for public and private transportation, and household consumption. Because the green hydrogen produced will be used on the combined cycle plant and as a material in syngas production, it will also contribute to the generation of renewable power for businesses and individual consumers. Synthetic gas has the same properties as natural gas, but its use ensures a decrease in net CO2 emissions.

MAJOR APPLICATIONS

Green hydrogen offers a wide range of applications due to its properties.

Fuel for the Transport Sector

Green hydrogen is widely used in transportation. The hydrogen generator that will be developed on our green hydrogen plant will be able to recharge networks of public or private transportation.

Industrial Fuel

The main consumers of green hydrogen are anticipated to be energy-intensive industries. As early as the first phase, the industry use will be able to prevail.

Clean Energy Generation

Because a portion of the power supply will be replaced with green hydrogen, the procedure will cut emissions from the power-producing process. The clean energy generated by a fuel cell will be available to businesses and homes.

Hydrogen Injection into the Existing Gas Network

Gas pipelines can be injected with green hydrogen. This means that with the help of the existing gas pipeline network, hydrogen injection may be used to supply homes and commercial industries.

Existing hydrogen applications where clean hydrogen can temporarily replace grey hydrogen generation, often with moderate modifications, and so eliminate the 830 Mt of CO2 being generated include:

Hydrogen Transportation, Storage, and International Trade

Today, most of the hydrogen is confined, meaning it is produced and consumed in the same area for sectors like ammonia manufacture and petroleum refining. As a result, while a certain part of hydrogen is supplied as compressed gas or liquid, the overall transportation and storage are quite minimal. Hydrogen conversion, transportation, and storage incur additional costs, which can be higher when hydrogen is used in smaller-scale distributed applications. As a result, massive, co-located, captive hydrogen production and storage often provide end-users with lower clean hydrogen costs.

Green hydrogen, in particular, is adaptable and enables flexible co-location and extension close to the hydrogen end-use. Although much hydrogen use can be limited, expanding hydrogen use across several industries would necessitate an improved transportation and storage system. The accessibility of suitable resources (e.g., low-cost renewable power or natural gas) and hydrogen storage locations may necessitate separate production and end-use in some circumstances. The cost-differential relative to local production and other local factors such as lack of available land area can affect the potential to transport the hydrogen from favorable production areas (i.e., low-cost zero-carbon electricity or natural gas) to end-user locations. In some cases, it is more beneficial to generate hydrogen in low-cost areas and transport it to higher-cost ones. Variations in renewable electricity pricing or physical availability between locations, on the other hand, can be balanced by transporting electrons over large distances in high-capacity HVDC cables. If inexpensive gas is used to produce hydrogen, it is economical to transport the gas and produce blue hydrogen closer to consumers rather than transporting hydrogen, assuming CCS (Carbon, Capture, and Storage) is available. In the near future, large-scale international energy trade will come in many different forms, reflecting local conditions as well as future technological and cost changes.

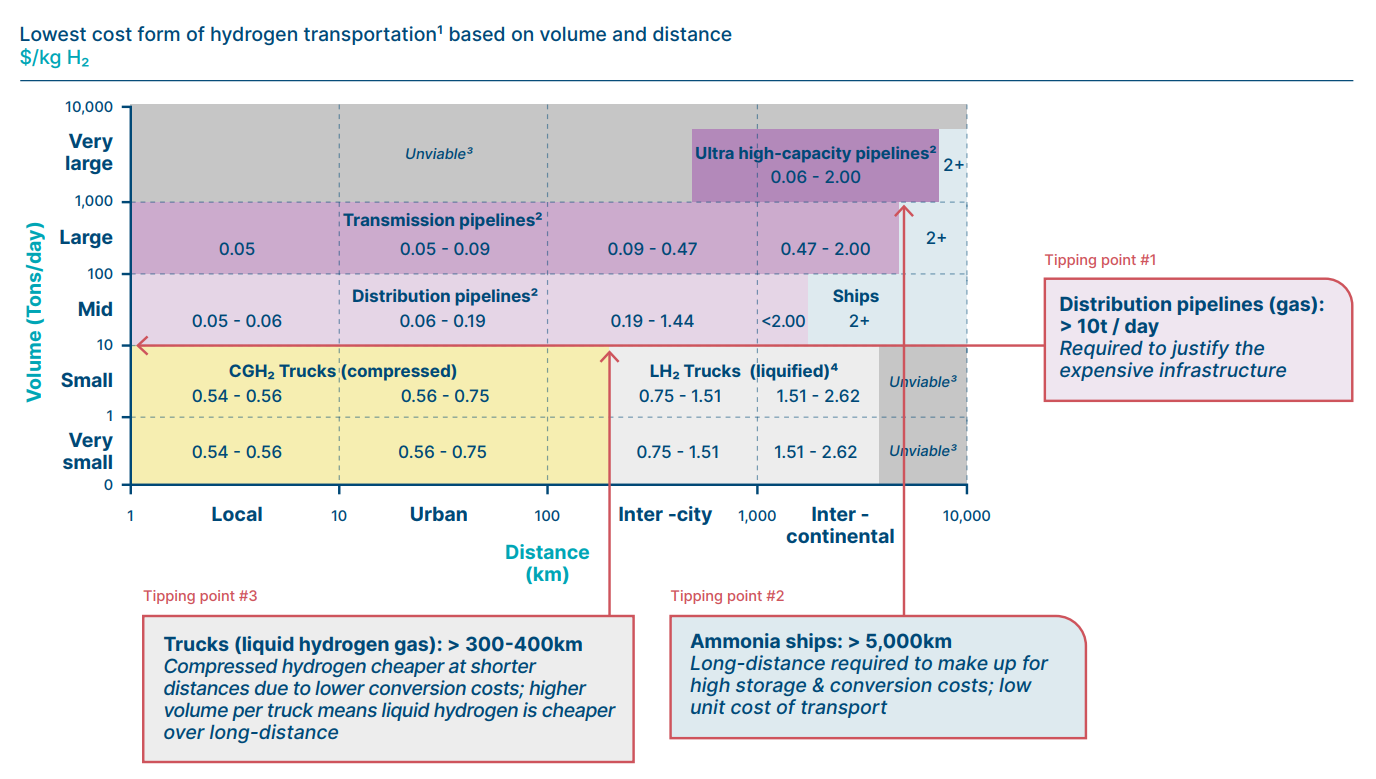

Hydrogen Transport Options and Costs

Hydrogen can be delivered in liquid form at -253°C or as a compressed gas at pressures up to 1000 bar. It can also be delivered in the form of hydrogen vectors like ammonia or liquid organic hydrogen carriers (LOHCs): the former is currently widely used; the latter has a lower TRL (Technology Readiness Level) and will require further development before becoming commercially viable. The overall energy loss ranges from 0.5-11 % for compression and decompression, and more than 70 % if hydrogen is transformed to ammonia and then restored to hydrogen before usage. However, if ammonia is utilized in the final application, the expense of conversion is not incurred.

The most cost-effective type of hydrogen to deliver is determined based on the volume and distance involved. Figure 7 shows the most likely lowest-cost solution as well as the cost per kilogram for various combinations. The expected breadth of application of certain technologies is defined by three important tipping points:

Although pipeline delivery of hydrogen is less expensive than shipping, especially when the end-use is hydrogen (due to high conversion costs), local green production is typically competitive.

Figure 7

- Pipelines: Once transportation quantities exceed 10 tonnes per day, pipelines are usually the most cost-effective form of transport. Lower-capacity distribution pipelines with capacities of less than 100 tonnes per day will be prioritized for local smaller networks, while transmission pipelines with capacities higher than 100 tonnes per day will be the most cost-effective way to transport large volumes over long distances. The cost of a transmission pipeline might range depending on distances. However, as the demand for hydrogen grows, ultra-high-capacity transmission lines might be built to transfer bigger quantities at a lower cost. Around 4500 kilometers of hydrogen pipelines are in use today, with the longest stretching 500 kilometers. Natural gas pipelines, on the other hand, cover 3 million kilometers. Refitting existing high-capacity gas pipelines to transport hydrogen is expected to cost between 40 and 65 % of the cost of new pipeline construction, depending on the exact materials used in the initial pipeline.

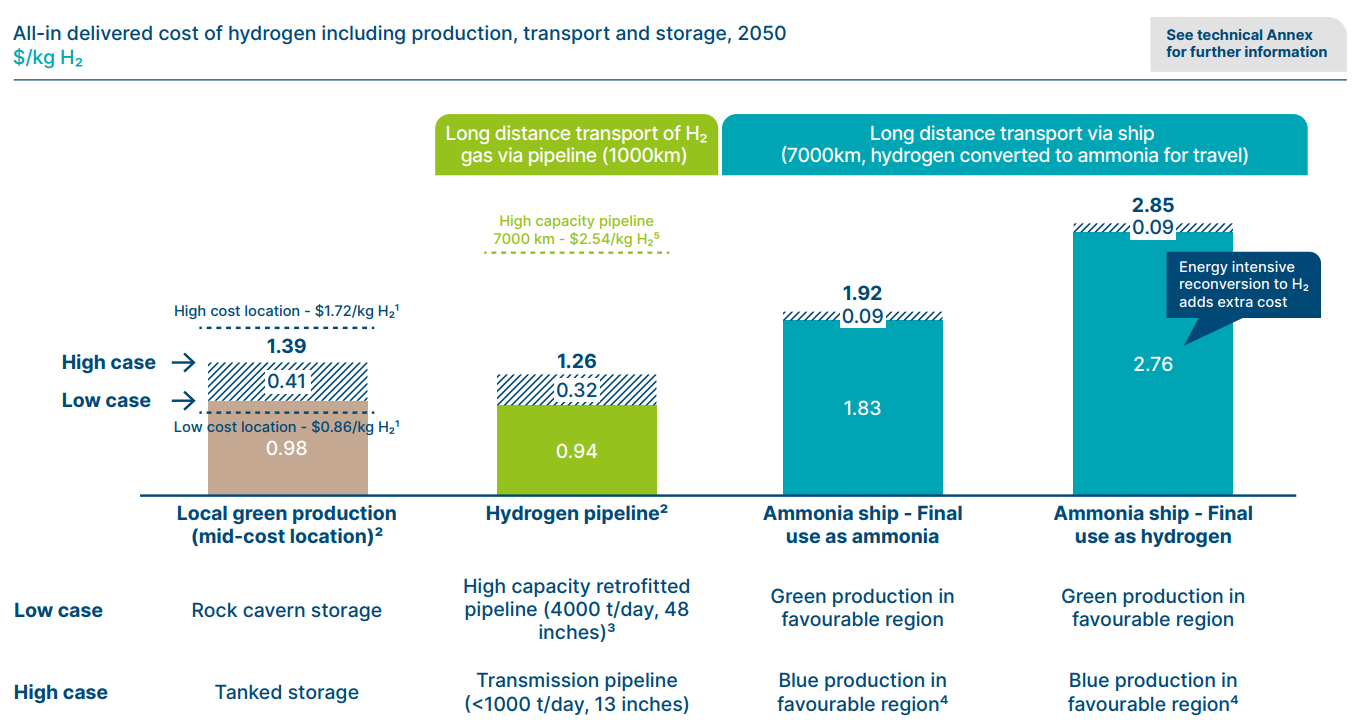

- Shipping: For international distances of thousands of kilometers needing large capacity (>100 t/day), transporting ammonia by sea is expected to be more cost-effective. As with the present international sea-based ammonia trade, shipping hydrogen as ammonia for end-users could be cost-effective across shorter distances. This avoids high-cost hydrogen restoration at the destination, thereby moving ammonia production to a different place (Figure 8).

- Trucking liquid hydrogen gas: Vehicles carrying compressed hydrogen are anticipated to be most competitive for smaller volumes and distances, although prices are currently challenging depending on the reached distance. For lower volumes over larger distances (hundreds of kilometers), liquid hydrogen vehicles are anticipated to be cost-effective, with costs rising as the distance traveled increases. To reach low-cost hydrogen for small-scale end users, these transportation costs must be reduced (e.g., refueling stations for use in long-distance trucking).

Although pipeline delivery of hydrogen is less expensive than shipping, especially when the end-use is hydrogen (due to high conversion costs), local green production is typically competitive.

NOTE: ¹ Green hydrogen production + low-cost rock cavern storage; ² Green hydrogen production takes storage costs of 50% annual demand into account. ³ Lowest cost retrofitted natural gas pipeline according to European Hydrogen backbone report. ⁴ Blue hydrogen production via ATR + CCS (90%+ capture rate). ⁵ Assuming medium leveled cost of Greenfield high-capacity pipeline according to European Hydrogen backbone report

Figure 8

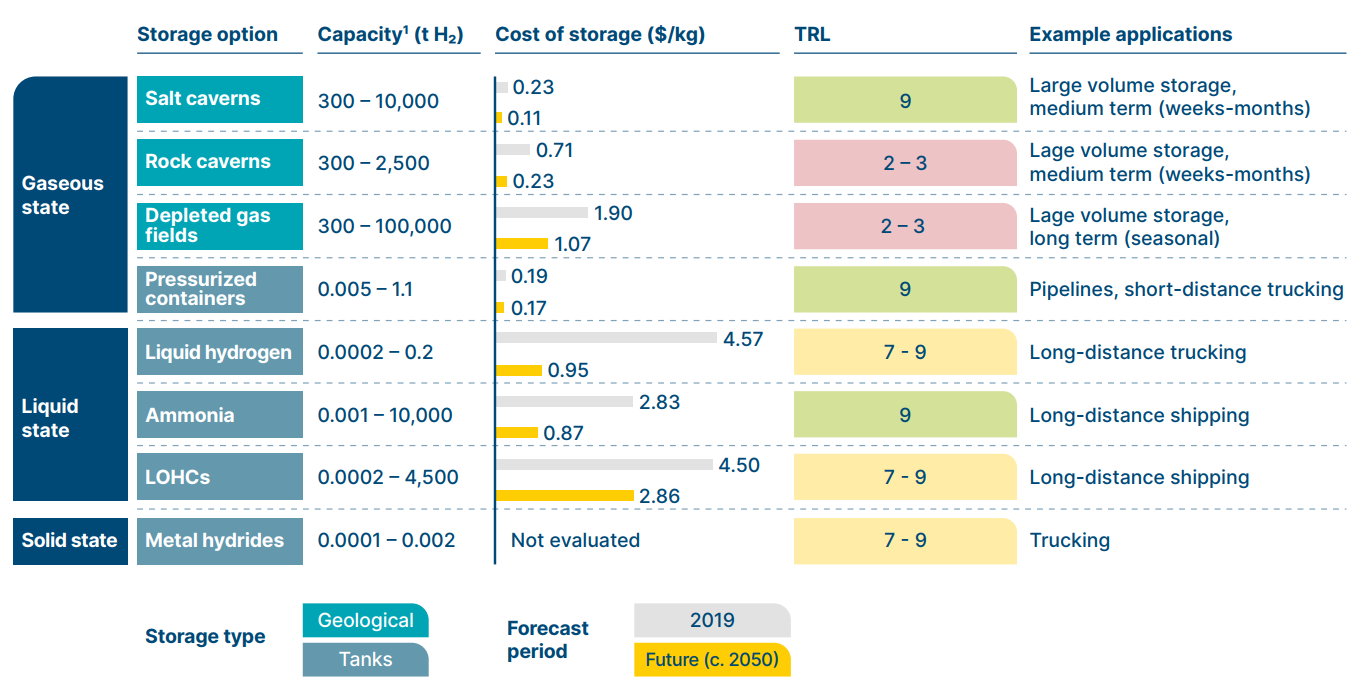

Storage Options and Costs

A hydrogen economy will necessitate a large amount of storage capacity. While the majority of current captive applications of hydrogen require little storage (since the consistent output of grey hydrogen production plants matches the steady inputs necessary for most industrial processes), many future uses of hydrogen (or hydrogen compounds) will necessitate storage, due to the fact that:

- Hydrogen's potential use in power networks is as an energy primary storage, with hydrogen being created when fluctuating renewable supply exceeds demand and is consumed when it is in short supply.

- Any use of hydrogen or hydrogen-derived fuels as a transportation fuel will necessitate the construction of major new storage and refueling facilities, such as in the road transportation sector, ports, and airports.

- Many industrial processes, such as ammonia synthesis or steel direct reduction, may require hydrogen buffer stocks to ensure continued operation in the face of fluctuating green hydrogen generation. In this situation, blue production would have the advantage of a consistent output profile, obviating the need for hydrogen storage.

Any use of hydrogen in domestic heating will necessitate buffer supplies of hydrogen, similar to today's natural gas reserves. While the worldwide natural gas infrastructure now has a storage capacity equivalent to around 12% of annual demand, it is projected that storage capacity equivalent to 15 to 20% of annual hydrogen use will be required. Because hydrogen's natural state volumetric density is just 30% as that of methane, it necessitates either extremely large-scale storage or the use of compression methods. By storing hydrogen in compressed gas or liquid form, the total amount of storage required can be minimized. However, the overall unit capacity of these storage forms makes them financially unviable for applications that demand a lot of storage. As a result, large-scale geological storage will be critical in the hydrogen economy. This could take three different forms:

- Salt mines, which can sustain the quantities and storage cycles necessary by large-scale industrial processes like steel manufacture. However, the availability of salt deposits varies significantly by region, therefore salt caves are not found in all areas. As a result, while switching from fossil fuels to hydrogen, the optimal location of some significant industrial operations may alter.

- Rock caverns are already utilized to store LNG (Liquefied Natural Gas) and petroleum products, but further research is needed to determine the economics and feasibility of using them to store hydrogen.

- Without enough purification, depleted gas and oil reserves, which might theoretically provide vast storage capacity where technologies are currently unproven, and the influence of contaminating elements will limit possible use in particular sectors (e.g., fuel cell applications).

If taking away the aforementioned, significant compressed storage in tanks or transportation infrastructure (to permit hydrogen supply from different locations) will be necessary. Future storage needs will be a challenge regardless of geography or local availability of low-cost geological hydrogen storage. Only about 100 major salt caverns are currently in use for natural gas, although 5% of predicted demand would necessitate around 4,000 large salt caverns.

Large-scale geological hydrogen storage is the most cost-effective, however small-scale storage costs are predicted to drop significantly.

NOTES: ¹ Capacity is “per unit” – IE: one salt cavern. Costs of hydrogen storage depends significantly on cycle rate (IE: how often the gas is filled and withdrawn). Geological storage of hydrogen is limited in how fast gas can be withdrawn (ca. 1 month for salt cavern).

It is clear that hydrogen can and must play a major role in the future zero-carbon economy, alongside massive clean electrification. The following points make it clear that the recent clean hydrogen revolution will materialize:

- Low-cost green hydrogen production is now possible due to declining prices and growing variable renewable energy generation capacity;

- The search for zero-carbon solutions is fueled by raising public awareness of climate change and national decarbonization commitments;

- Net-zero targets and legislation place a greater emphasis on difficult-to-abate sectors where direct electrification is not usually viable and hydrogen is frequently required;

- Significant green recovery funds have been set aside to accelerate the development of clean hydrogen.

The objective is to improve clean hydrogen production and delivery in order to enable low-cost production and develop the industry so that the outcome is decarbonization by 2050. This will require:

- Obtaining sufficient scale early enough to reduce the cost of green hydrogen production by ensuring that announced projects are completed within the next decade;

- Ensuring that demand grows quickly enough to enable decarbonization by 2050 – this will necessitate explicit regulations to boost the use of clean hydrogen in some critical areas;

- Ensuring key technology investments – the most important for green hydrogen is major electrical system development, while assistance for CCS infrastructure development will be required for blue hydrogen;

- Using specialized hydrogen clusters to drive integrated development of production, end-use, transportation, and storage to build up the clean hydrogen value chain in a coherent manner;

- Long-term planning for national and international transportation and storage requirements;

- Developing adequate safety and quality standards, as well as social approval and certification systems for clean hydrogen.

Cost Decreases at a Critical Scale and Pace

In the long run, green hydrogen costs will certainly outperform blue hydrogen costs in most regions. The costs are related to the high capital expenditures of electrolyzers as well as the usage of expensive electricity and the limited scale of green hydrogen projects. Once the green hydrogen developments that have already been proposed by governments and corporations materialize, green production prices might fall, making it competitive with blue in some regions and grey in some others. Even in low-cost regions, the most advantageous locations for green hydrogen production may be cheaper than blue hydrogen, while intermittent green production storage costs could increase. The capital cost of electrolyzers and the cost of low/zero-carbon power dictate the price of green hydrogen. Both are rapidly decreasing, and low electrolyzer costs make it easier to obtain cost-efficient electricity.

Electrolyzers Costs

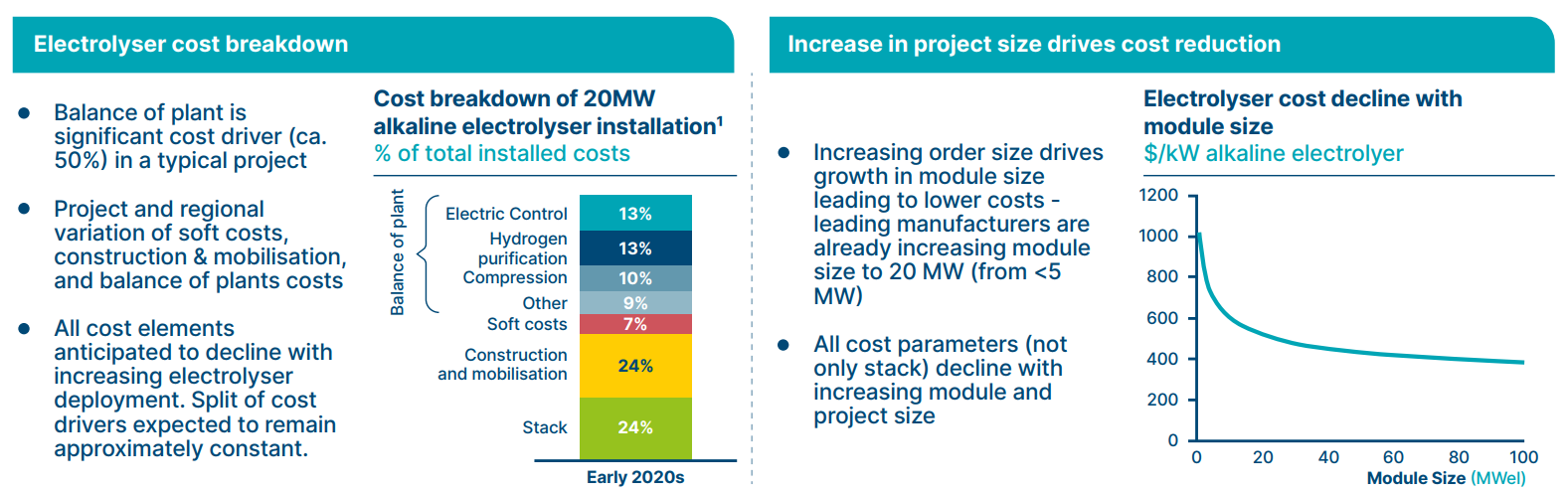

Electrolyzers costs are anticipated to fall due to economies of scale and learning curve effects. By 2030, learning rates and economies of scale associated with capacity should reduce fully installed alkaline electrolyzer costs.

Furthermore, the energy required to produce green hydrogen (i.e., electrolyzer efficiency) will drop in the coming years, from approximately 53 kWh/kg of hydrogen to approximately 45 kWh/kg of hydrogen, or even lower, due to technological innovation.

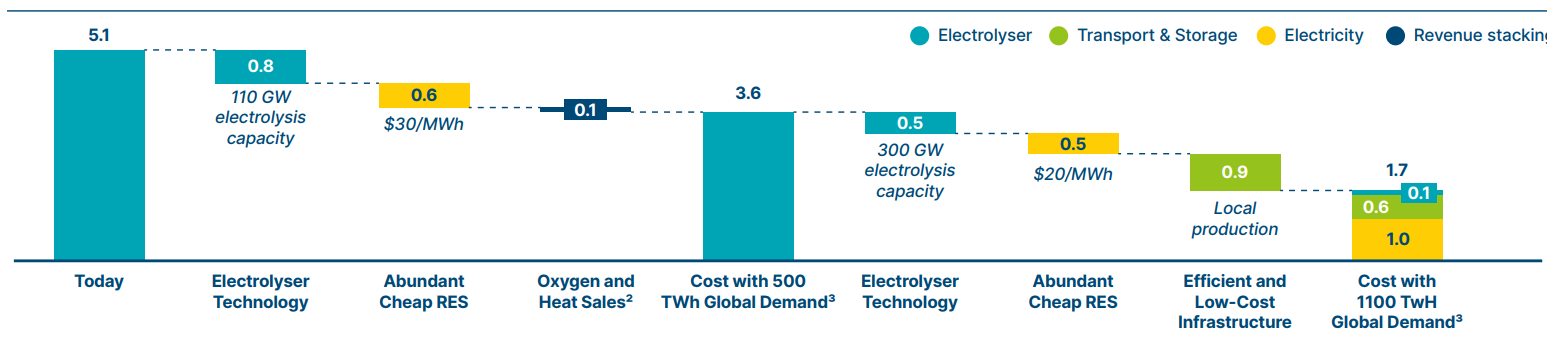

Figure 9

NOTES: ¹ Total cost of project $780/kW. ‘Soft costs’ include project design, management and overhead. ² 40% of oxygen and 20% of heat sold. ³ 500 TWh corresponds to ca. 10 Mt and 1100 TWh represents ca. 22 Mt. Assumption: 50 kWh/kg energy consumption for electrolysers.

What is needed to get to below 2 €/kg green hydrogen (in Europe)

LCOH €/kg H₂ delivered

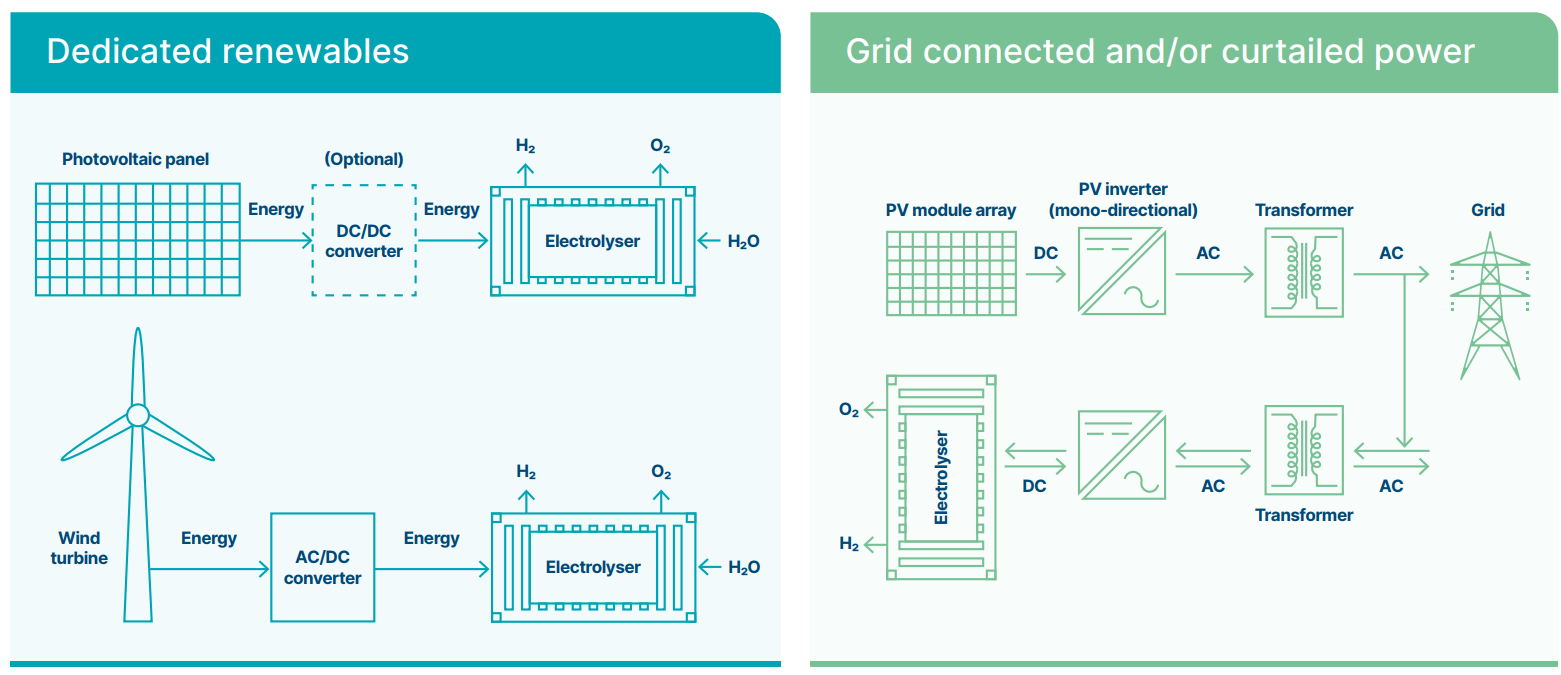

LCOEs (Levelized Cost of Energy) from dedicated renewables can be up to 15% lower than grid connected generation due to savings in power electronics

Due to cost savings in power electronics, LCOEs (Levelized Cost of Energy) from dedicated renewables can be up to 15% lower than a grid-connected generation.

High electrolyzer costs in the past made it necessary to run electrolyzers at full capacity in order to lower capital costs per unit of production, which meant relying on more expensive grid power. However, as the cost of electrolyzers falls, high utilization will become obsolete. As long as utilization rates are above roughly 2000 hours per year, and electrolyzer costs fall, electricity costs become almost the sole determinant of green production costs. As a result of the reduced cost of electrolyzers, green hydrogen production will be able to employ low-cost power from either:

- Dedicated low-cost renewables, in an environment where wind and solar LCOEs are expected to decrease in more favorable regions;

- Low-cost renewables that generate for a longer period of time, enabling increased electrolyzer utilization (such as offshore wind or solar-wind hybrids), with production costs subsidized by power sold to the grid when prices are high. Green hydrogen production costs could be further reduced by revenue stacking from complementing services, such as the selling of oxygen bi-product for oxy-combustion or the sale of power network balancing services.